FTX Trading Ltd.

FTX CEO John Ray’s first day declaration was one of the wildest bankruptcy filings I’ve ever read. Alongside the dramatic and entertaining quotes was the striking lack of real information about the debtor. Since then, we’ve learned a lot more about the operations of FTX and Alameda and the estate’s remaining assets, yet some of the most basic numbers are still unknown. Some of the information we’ve learned about the debtor’s operations and recent motions in the Celsius bankruptcy also suggest a narrower range of process outcomes.

The task at hand is to see if we can piece together some info, see through the fog, and estimate a range of recovery outcomes for FTX claims. Although the situation has generally captivated anyone with an interest in finance, technology, or fraud, (hard to argue the situation is “off-the run,”) given the weirdness of crypto assets, the large information gaps and the complexity in sourcing customer account claims, I think it’s a worthwhile exercise. As Ben Graham said, “you don't need to know a man's weight to tell him he's fat.”

Some ruminations on the events leading up to the Chapter 11 filings:

I first encountered crypto as a way of ordering drugs on the internet. I had heard about Silk Road on reddit and wanted to understand how it worked: so, I downloaded Tor, bought some BTC on Coinbase and went shopping. Looking back, and considering the current BTC price levels, the implied USD-cost of what may or may not have been purchased makes me a little sick. As did some of the other products and services on offer on the dark web, which compelled me to stick to offline commerce for my psychopharmaceutical purchases.

Thereafter, as a casual crypto observer, my interest in the space seemed to flare up every 6 to 12 months when a friend would describe a new “tokenomics” white paper or a novel DeFi business model. Even though I had watched several friends get rich, I resisted dedicating serious time or capital to the space, as the “pre-mortem” exercise of visualizing myself losing my money speculating at the top of a bubble seemed too real. It was obvious to many that the space was full of fraud and excess but, aside from small-time grifts, it wasn’t obvious to me where exactly the leverage was in the system.

My interest in crypto was piqued again in late May of last year, after the dominoes started to fall, beginning with the Terra (LUNA) implosion. Post-LUNA, it quickly became clear that the crypto ecosystem was undergoing a mini-financial-crisis. This crisis had certain financially unprecedented characteristics (e.g. digital assets, smart contracts, blockchain records), but closely mirrored historical analogs—fallout from explosive growth fueled by unsustainable customer deposit rates (S&L Crisis), deflation fueled deleveraging (the Great Depression, Japan 1990), and interconnected failures through unregulated shadow banks (2008 GFC). I closely followed the bankruptcy cases of Voyager and Celsius, in part because some of the legal issues of how crypto assets would be treated in the context of a Chapter 11 process were philosophically interesting. Also, I had previously met Celsius founder Alex Mashinsky[1].

While the rampant fraud in the crypto space was unravelling on a near daily basis, I was (and am still) convinced by some arguments for DeFi’s utility: much of the infrastructure underlying the global financial system is certainly inefficient and burdened by technical debt. And, as I discovered in my Silk Road adventures, most people won’t have the patience or technical expertise to interact with DeFi protocols directly, and so CeFi platforms will naturally emerge as user-friendly bridges to the underlying technology.

As SBF went on his “strong hand of crypto” media tour, I also saw certain favorable parallels in some of the early days of cable. Through the 80’s and 90’s, John Malone organically grew TCI’s base of cable subscribers and, by leveraging the cash flows of those subscribers, TCI acquired its way to become the largest cable provider in the US. However, where Malone captured the most value was in financing content: by offering fledgling cable networks a fully scaled subscriber base, he was able to invest early at highly attractive valuations, e.g. starting BET with a $500,000 investment. These deals in turn strengthened TCI’s content offering to subscribers, increasing organic sub growth, increasing cash flow available to expand TCI’s network, to acquire rivals and to invest in more content. Later, the FCC curtailed the co-ownership of distribution and content assets.

I thought the ecosystem that SBF created was similarly set up to capture enormous value in an emerging yet-to-be-regulated technology space: retail and institutional clients would choose to trade on FTX, which offered better liquidity through Alameda’s trading flows, the best venture projects would want the support of FTX and the chance to have their token widely adopted on the exchange, and Solana could be the L1 backbone for those projects. For the overall ecosystem to create and capture value, it didn’t necessarily imply that each part would be profitable on a standalone basis. One could even argue that if Alameda lost a small amount of money every year it could be enormously accretive for the ecosystem overall.

The problem was, in retrospect, Alameda was not doing “arbitrage” but rather likely blew-up in some number of ponzi-like trades, while investing stolen FTX client money in all sorts of illiquid venture and fund investments, while employees of FTX spent more stolen client money indiscriminately. I won’t review the blow-by-blow with Binance here, but a mere two months after David Rubenstein interviewed SBF, during which Rubenstein asked Sam how it felt to be compared to Pierpont Morgan, FTX froze withdrawals on November 8. The Bahamas government placed FTX Digital Markets, FTX’s Bahamas subsidiary, into liquidation on November 10. And John Jay Ray III, who took over as CEO of FTX, filed for Chapter 11 in the US on November 11.

A review of the key issues:

Ray’s first day declaration described the debtor’s org chart, breaking FTX into four groups of business referred to as “silos,” noting that SBF held majority economic and governance control of all four silos: the WRS Silo (FTX US), the Alameda Silo, the Ventures Silo (broken down into three main investment holding entities), and the Dotcom Silo (non-US FTX). A description of operating subsidiaries, non-debtor entities and a simplified balance sheet was given for each silo. The latter recreated below:

As FTX did not keep appropriate books and records or security controls, was missing bank account information, lacked centralized control over cash management and lacked proper auditors, much was left out of the above. Most notably: balances of customer crypto assets deposited were not recorded (…) on the balance sheet and are not presented. Which brings us to our first key issue:

Key issue #1: The denominator?!

Shortly after FTX filed Chapter 11, there was a wide range of estimates about what the total amount of customer deposits actually was. We now know there were about 9mm customer accounts, but still not the total deposit figure. SBF himself noted it was about $8.5bn, which roughly matches an $8bn figure corresponding to the loan from FTX to Alameda in the initial SEC complaint. The WSJ noted here the number was closer $10bn.

The highest number I’ve seen was $16bn, for which I can’t locate a real source, and seems to possibly refer to the peak-amount of customer deposits. SBF was apparently trying to raise equity prior to the collapse noting roughly that figure, which was further cited as a peak figure in the CFTC report and we know (from the SEC complaint) that on November 9 (pre-petition) that FTX customers withdrew about $5bn that day. We really don’t know the answer, and it could be very damaging to recoveries, if substantially higher, but I’m inclined to believe that if the figure was materially higher, we would have heard by now. To be somewhat conservative, we can start with a range of $9-11bn of customer deposit claims across the FTX & FTX US entities (WRS & Dotcom Silos). Which brings us to our second issue:

Key issue #2: Substantive consolidation

The balance sheet table above, pulling from the FDD disclosures, also excludes intercompany accounts receivable, accounts payable, loans payable, and loans receivable, of which there are many. Notably several multi-billion-dollar intercompany claims Alameda and WRS have on the assets of the Ventures silo entities.

A constant refrain from SBF, post-implosion, is that FTX US could “pay all customer withdrawals tomorrow,” and that, if not for the Chapter 11 filings, FTX US would have been just fine. Initially many potential sellers of FTX US claims believed this to be generally true. However, the CFTC investigation revealed that “assets flowed freely between the entities, often without documentation or effective tracking.” FTX and Alameda shared office space, key personnel, technology and hardware. Around November 7 or 8, according to the CFTC, FTX executives discovered a shortfall at FTX US that they “did not understand and were unable to quantify.” Additionally, what is clear from the SEC’s civil complaint is that the misappropriation of customer funds wasn’t a one-off thing. This was a “brazen, multi-year fraud.”

To me, it seems difficult for the court to not smush everything together, i.e. substantive consolidation. Pulling from an old Jones Day memo, substantive consolidation is appropriate as an equitable remedy when: (i) there is substantial identity between the entities to be consolidated; and (ii) consolidation is necessary to avoid some harm or to realize some benefit.

Factors that may be relevant in satisfying the first requirement include:

Fraud or other complete domination of the corporation that harms a third party;

The absence of corporate formalities;

Inadequate capitalization of the corporation;

Whether funds are put in and taken out of the corporation for personal rather than corporate purposes;

Overlap in ownership and management of affiliated corporations;

Whether affiliated corporations have dealt with one another at arm's length;

The payment or guarantee of debts of the dominated corporation by other affiliated corporations;

The commingling of affiliated corporations' funds; and

The inability to separate affiliated corporations' assets and liabilities.

I would be interested to hear a compelling argument to the contrary, but it seems like customer claims should be treated as one creditor group. Tellingly, while the first day declarations spent a lot of real-estate on the corporate structure, a number of the disclosures from the estate’s advisors have since talked about the assets framed in a more consolidated way.

Key issue #3: Customer claim seniority

The question is: will customer account claims be GUC’s or be senior to other claims? Returning to the FDD disclosures: there are about $7.8bn of liabilities (excl. customer claims), or about $5.5bn, excluding related party liabilities. Most of these are obviously GUCs, although the largest bucket: the $3.9bn of “crypto asset borrowings” roughly correlates with the ~$4bn of assets sitting on the Alameda balance sheet. To my knowledge no loan documentation has been made public on these, but for the moment let’s assume those net out (implying that they’re secured).

The best overview of the relevant issues here is Adam Levitin’s aptly named Not Your Keys, Not Your Coins, which gives an overview of how customer deposits at cryptocurrency exchanges may be treated in bankruptcy, notably whether or not cryptocurrency assets will be treated as property of the estate (and thus subject to the automatic stay), the types of relevant trust structures, the applicability of UCC Article 8 and the characterization of crypto assets as bailment.[2] Levitin is fairly pessimistic on the treatment considering the options and the language in crypto exchange user agreements, noting the potential uncertainty of state law applying a constructive trust structure and the confusing applicability of Article 8 (even in the case where all the non-stablecoins tokens fall under securities law). Levitin does note that the uncertainty exists in part because of a lack of case law and I think the Court’s actions in the Celsius case with respect to the issue of the so-called Custody Accounts is instructive[3].

Much of the backstory is described nicely in the interim examiner report[4]: Following a cease and desist letter from NJ state regulators claiming that Celsius’ main product, Celsius Earn accounts, were, in fact, unregistered securities offerings, Celsius invented the Custody program where, according to the Terms of Use, the title of crypto assets remained with the customer and customers couldn’t earn the same monetary rewards on deposits as they had previously enjoyed under the Earn program. In contrast to the configuration of the new product, the examiner report goes through enormous and entertaining detail to show how assets were comingled and that the Custody Accounts were really custody in-name-only.

And yet, in a December 7 hearing, Judge Glenn verbally authorized Celsius to release Custody Account assets back to customers. “There is no preference,” he said. “There is no good faith argument of an avoidable preference against them. There is no dispute as to their having title, and the assets should be returned to them.” No discussion of constructive trust, UCC Article 8, etc.—the language in the Terms of Use was decisive and the debtor, the UCC, and the ad-hoc account holders all agreed.

FTX’s most recent Terms of Service, states "You control the Digital Assets held in your Account. Title to your Digital Assets shall at all times remain with you and shall not transfer to FTX Trading (…) None of the Digital Assets in your Account are the property of, or shall or may be loaned to, FTX Trading; FTX Trading does not represent or treat Digital Assets in User’s Accounts as belonging to FTX Trading." Fiat deposits could be treated differently. Fiat depositors are credited with FTX’s electronic money, implying FTX takes the title of the fiat deposits. As title holder, FTX can do whatever it wants with fiat deposits as long as depositors get their money back when they ask for it.

Although it’s far from a sure thing, I’m inclined to believe the court will treat FTX account holders according to the Terms of Service, i.e. that stealing customers deposits was, in spirit, a breach of trust, and the point of maximizing the value of the estate should be to remedy that loss, i.e. that customer account claims will be senior to other unsecured liabilities.

The uncertainty of the treatment of crypto assets in Chapter 11 could also theoretically cut to the benefit of claimants: if the estate will be substantively consolidated and the ~$4bn of crypto assets on Alameda’s balance sheet are actually worth anything, I wonder, by what contract are they secured against their corresponding liabilities? How can DeFi liens be perfected? Questions worth asking from the perspective of GUCs and account holders alike.

Key Issue #4: What value remains for creditors?

To start with: some cash & crypto. In early January, the estate gave an update. The headlines read something like “FTX recovers $5bn in assets.” The details are less positive: looking at PWP & S&C’s presentation to the UCC from January 17, we see that there is $1.7bn in cash. But here we should net out non-debtor cash of $163mm belonging to LedgerX and $164mm of custodial cash at FTX Digital Markets.

Further: of the $3.3bn in liquid crypto assets, the largest category was defined as “crypto held at 3rd party exchanges.” Pulling from the deck, “the Debtors currently have limited visibility into the token composition of crypto balances at certain 3rd party exchanges. Once obtained, information provided by these exchanges is likely to increase the balances of certain tokens listed here.” Given the counterparty risk in the space and the unknown nature of the tokens, I’ll say this isn’t worth much right now. And, aside from that, there’s only $268mm of BTC, $90mm of ETH, $245mm of stablecoins and a ton of other tokens[5].

As for non-liquid assets, there have been a few attempts to compile an exhaustive list of all the investments FTX made (here is one). The largest 30 investments comprise 80% of the nearly $5bn cost-basis list, followed by a long tail of ~400 smaller checks[6]. Looking at the first bucket: there’s a lot of crap, but a few assets to highlight:

Anthropic: Anthropic is an AI startup founded by former OpenAI employees in 2021. FTX led Anthropic’s monster series B round with a $500mm investment. Even a few months ago I would have written this off as a zero, but following the venture hype-cycle rotation into AI, Google just invested $300mm into the business (undisclosed valuation). This very well could be a zero and it would be quite the rollercoaster if a reckless investment in a speculative AI start-up bails out fraudulent crypto exchange customers.

K5: FTX committed $300mm to a firm called K5 Ventures. I had never heard of them before this, but looking at their website, it doesn’t seem like a total fraud. Further, it would have been difficult for them to put all that money to work. Obviously, it deserves a discount, but likely worth something material.

IEX: Of Flash Boys fame. FTX acquired a $270mm stake in early 2022. No clue on the valuation, but I’ve been told by at least one person in the HFT world that IEX is a reasonably sound business and not a fraud.

Pionic (TOSS): FTX invested $113mm in this Korean fintech “super-app” at a ~$9bn valuation in 2022. It looks like they’ve raised since, so I’m willing to say it’s not a fraud and probably worth something material.

Sequoia & Sequoia Heritage LP: Apparently SBF committed $100mm each to Sequoia and Sequoia Heritage, the family office of the Sequoia partners. Interestingly in their post-mortem press release, Sequoia failed to mention whether or not they received the money. Googling around doesn’t help. My bet is they received the cash, but perhaps they did not.

In total, the cost basis of these five investments amounts to $1.4bn. We can and should haircut this amount in the sensitivity analysis. There are also some very large zeros in the top-30 list, among the more ridiculous: a $550mm investment in Genesis Digital Assets, a BTC miner in Kazakhstan, $400mm in two subscriptions to Madulo Capital, which looks like SBF’s buddy living in the Bahamas, a $100mm convertible PIPE to Dave’s SPAC deal, all the Voyager cash lit on fire, etc. Beyond the top-30, the cost basis for the ~400 smaller checks amounts to nearly $1bn, which should be heavily discounted as they were mostly seed and early stage venture crypto investments done at the top of the market[7].

Amazingly, we’re still finding out about checks SBF may or may not have written, e.g. Elon Musk invited him to roll the $100mm stake he had (allegedly) owned for a few months into a privately held Twitter. And, according to an FTX balance sheet prepared after the takeover closed, on October 28, and circulated to investors listed Twitter shares as an “illiquid” asset.

There are also assets that seemed to be in limbo to the estate, most notably the Robinhood shares: SBF appears to have pledged the same shares as collateral for multiple loans. BlockFi, FTX creditor Yonathan Ben Shimon, FTX led by John Jay Ray, and SBF himself, all claim ownership.

The estate also wants to sell FTX subsidiaries, starting with LedgerX, FTX Japan, and FTX Europe AG. Similarly, I’m counting these all as zeros. LedgerX has been hailed in various places as “legit,” but based on the financials filed on the docket, it seems like another cash hemorrhaging joke. FTX Europe had a cost basis of $320mm, but who knows.

Key Issue #5: Clawbacks, etc.

There’s also the issue of “clawbacks.” I think there’s probably two things here: (i) preference claims to accounts that withdrew assets leading up to the bankruptcy filing and, less materially, (ii) equitable subordination of insiders. We know from a number of disclosures that there was at least $5bn in withdrawals right before the Chapter 11 filing. I would bet the preference pool is much larger than that. The actual recoveries to the estate will be much lower than face amount as each preference action requires litigation (and the lawyers usually keep 1/3 of the proceeds) and they expand the claims denominator of course.

What amount of the total ~$10bn of customer claims were either employees of FTX or were large crypto funds who were given the privilege of becoming equity owners of the platform? We don’t know but it’s likely material and they could be subordinated to other customer claims. There’s also the Bahamas-back-door incident, which stinks of corruption, bribery, etc.

Finally, as pointed out by (of all people 3AC-founder-on-the-run-from-Singaporean-law-enforcement) Mr. Zhu Su, there’s likely going to be a substantial reduction in the claims pool from the ineligibility of customers who were falsifying their KYC information.

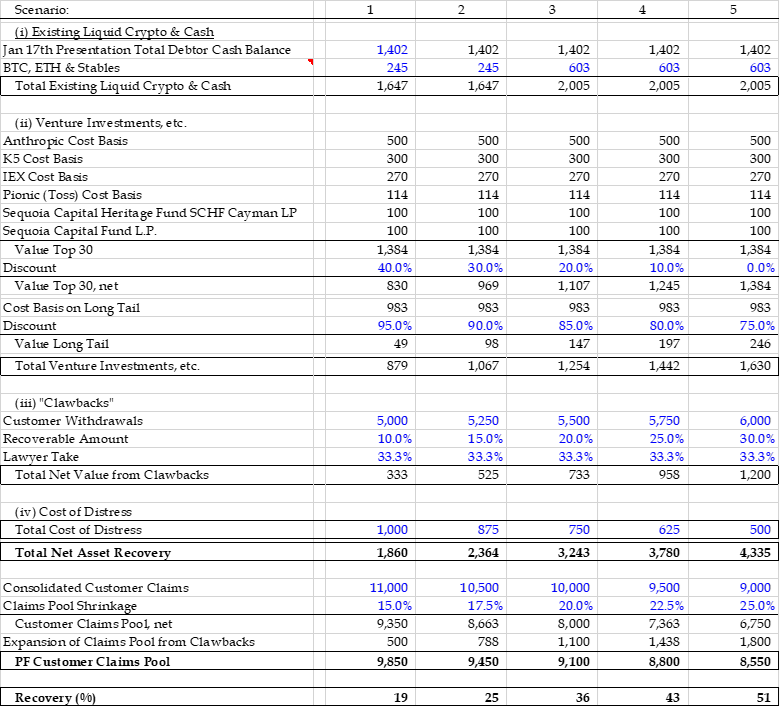

Valuation— Putting it all together:

Here’s a back of the envelope sensitivity with all we discussed:

Moving part-by-part: We’re counting the total Debtor cash ($1.4bn), plus the BTC, ETH and stablecoins identified, only counting the stablecoins in the lower cases. This amounts to $2bn in the base case.

Considering the value from the venture portfolio, we’re taking the five investments reviewed earlier with a cost basis of $1.4bn and discounting that up to 40%. Perhaps you could argue the discount should be more. Then we’re adding the nearly $1bn-cost-basis on the long tail of venture investments, discounting 75-95%. This amounts to $1.2bn in the base case (roughly just above a 20% recovery from cost basis).

We then add in $5-6bn of clawbacks at a 10-30 cent recovery, netting a third of the clawback value for lawyers’ fees. That implies an incremental >$700mm in value at the midpoint.

We must deduct what will surely be an impressive cost of distress. For all the articles noting Mr. Ray’s working class background and high-minded ideas of justice, he’s going to make a hell-of-a-lot of money on this transaction, as will basically every professional involved[8]. We can triangulate using cases like MF Global (>$750mm) and Madoff (>$1bn), but your guess is as good as mine. Here I’m using $500mm-$1bn.

Net of bankruptcy costs, the math here implies total net assets of $1.9-4.3bn. And, to get to our recoveries, we should adjust the ($9-11bn) claims pool for the clawbacks mentioned earlier, but also shrink the claims pool for KYC and other reasons that claims go unfiled (here I’m using a range of 15-25%). Net we’re getting to a pro-forma claims pool of $8.5bn to just under $10bn—implying recoveries of ~20-50 cents on a wide range. I think a base case expectation of a mid-30’s to low-40s recovery seems about right.

So, what’s the price? Claims brokers have most recently told me that the market is in the high-teens/low-20’s. The market for individual claims will vary quite a bit given counterparty issues, documentation issues, and even claim size. If you could get your hands on paper in that context, it seems like an attractive bet. Given the amount of cash and crypto on the balance sheet and asset sales proceeds coming into the estate, I imagine you could get a large portion of your recovery within two years, making the IRRs quite attractive. This comes with the obvious caveat that inter-creditor group fighting around the substantive consolidation issues and seniority of customer claim might delay distributions quite materially.

[1] In 2014, Mashinsky was appointed CEO of a company called Novatel Wireless. Novatel primarily made the WiFi hotspot “MiFi” boxes sold through Verizon—a secularly challenged business that was attempting to pivot into telematics applications. Novatel had raised a convertible bond to fund the business turnaround and I remember walking out of Mashinsky’s roadshow presentation remarking to my boss at the time that, although Mashinsky seemed a bit too promotional for my tastes, if 20% of what he said was true, this would be a great investment (it was, in fact, closer to 0%). We had met a few more times in New York before the Novatel board fired him, not more than a year later, after which we lost touch. Six or seven years later, I was shocked to see his face on the front cover of the FT wearing a shirt that read, “Banks are not your friends,” operating this CeFi platform that boasted >$25bn of AUM.

[2] The whole paper is worth a read. In one of the funnier footnotes I’ve read: Levitin points out that the only cryptocurrency user agreement he saw that invoked Article 8 of the UCC was the June 1, 2022 version of the Coinbase user agreement. And, shortly after the public circulation of a draft of Not Your Keys, Not Your Coins, Coinbase changed the user agreement to exclude the language.

[3] There’s other supportive case law outside the US, notably Quoine and Cryptopia

[4] Also, an amazing read.

[5] This includes $685mm of Solana—given the integration with the SBF ecosystem and unproven utility of Solana as an L1 token, I write this off too. Perhaps the latter point should apply to ETH as well. These totals are also using token prices as of the filing date. They also exclude $140mm held at FTX Japan, any securities like the $197mm of GBTC held in an Alameda brokerage account, AND the $415mm of crypto SBF someone stole through a hack just after FTX imploded.

[6] There’s also real estate in the Bahamas with a cost basis of $253mm, including the polycule’s penthouse at the Albany Marina Residence.

[7] On the last point here. We should of course discount the portfolio heavily. However, my thoughts earlier re:the FTX flywheel and the nature of venture cap selection bias lend some credence to this portfolio probably being pretty attractive for the buyer that wants a diversified venture bet in crypto. If (a big-if) Web3 is going to be a real thing, it’s probably a pretty interesting bet.

[8] In SBF’s overture to the Voyager estate, he noted the excessive costs of professional fees in Chapter 11—not everything he said was BS.